Covered California Premiums for 2019 Increase Amid Concerns that Federal Efforts to Weaken the Affordable Care Act Are Having an Impact

By Elia Gallardo

Last week, Covered California announced preliminary health plan premium rates for the 2019 coverage year and suggested that federal action to weaken the Affordable Care Act (ACA) may have yielded higher rates than might have otherwise been expected. Subject to approval by state regulators, Covered California 2019 individual market rates will increase on average 8.7 percent.[i]

According to Covered California, as much as 2.5-6 percent of the increase can be traced to Congressional action weakening the ACA requirement for individuals to maintain coverage through federal tax legislation at the end of 2017 which reduced the tax penalty to zero starting in 2019. This is because the absence of a financial penalty discourages younger and healthier individuals from buying coverage, deteriorating the overall risk mix and increasing the average costs for those who remain enrolled. Covered California projects 262,000 primarily young and healthy Californians will drop coverage in 2019 with premium impacts likely to extend beyond next year.

Recognizing the increase associated with the elimination of the mandate penalty, the announced premium rates otherwise reflect relatively modest increases in the cost and usage of medical services and products, and a generally stable individual market. Steady enrollment projections and an overall healthier risk mix than markets in other states are preventing California from experiencing the double-digit rate increases expected throughout the nation. All eleven existing Covered California health plans will be offering coverage again in 2019.

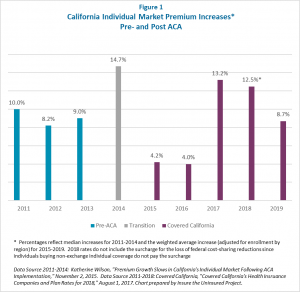

Premium Growth is Slower on Average than in the Pre-ACA Individual Market

While the anticipated rate increases are significant enough to intensify affordability challenges for some consumers, especially those not eligible for federal premium assistance, the projected premium increases are lower on average than those in the pre-ACA individual market. As Figure 1 illustrates, the pre-ACA median premium increase in California’s individual market from 2011 to 2013 was 9.2 percent per year.[ii] The average change for Covered California from 2015 to 2019 is 8.4 percent.[iii]

Pending Federal Action Could Impact Future Premiums

Lawsuits and federal administrative actions have the potential to adversely impact health plan premiums in future years.

In one high profile case, multiple states have challenged the constitutionality of the individual mandate and further argued that the entire ACA must be struck down if the individual mandate is found to be unconstitutional. The basis for the states’ objection to the mandate is the federal Supreme Court ruling in 2012 that the coverage requirement was constitutional as a tax provision. The states argue the Court’s rationale no longer applies in the absence of a real tax penalty.

The federal Attorney General sided with the plaintiff states on the constitutionality of the individual mandate and refused to defend portions of the ACA in court. The Attorney General argued in court filings that in addition to the coverage requirement, community rating and protections for those with preexisting conditions should also be struck down. Community rating prohibits insurers from setting rates based on health status, medical claims, or gender.

Most recently, the Centers for Medicare and Medicaid Services (CMS) created additional uncertainty for the ACA marketplaces by suspending and then reinstating 2017 payments for insurers participating in the ACA market stabilization program known as risk adjustment. Risk adjustment transfers funds from health plans with lower-risk (lower cost) enrollees to health plans with higher risk (higher cost) enrollees. The ACA risk adjustment program applies to individual and small group insurance markets (except for grandfathered plans that existed at the time of ACA enactment.) On July 24, 2018, CMS announced that they would make the transfer payments to eligible health plans beginning in October 2018. Plaintiffs in several lawsuits have also questioned other ACA programs intended to support insurer participation in marketplaces, including the risk corridors programs, a temporary program in place 2014-2016.

California policymakers will need to carefully monitor federal developments and consider the potential impacts for California. Over the last couple of years, California adopted several workarounds to protect the state’s coverage gains, including, for example, a longer open enrollment period than federally required and increased funding for outreach and enrollment in the wake of federal reductions in outreach funding. It may be necessary for California to take additional steps in 2019 to mitigate the impacts of federal policy changes and to preserve the relatively stable and strong individual market in the state.

Stay tuned!

[1] Covered California, “Covered California Releases 2019 Individual Market Rates: Average Rate Change Will Be 8.7 Percent, With Federal Policies Raising Costs,” Press Release, July 19, 2018.

[2] Katherine Wilson, “Premium Growth Slows in California’s Individual Market Following ACA Implementation,” November 2, 2015. ITUP calculated the 2011-2013 average using the data, adjusted for the number of enrollees in each year, in the table titled, “California Individual Market Premium Increases.”

[3] Covered California, “Covered California Releases 2019 Individual Market Rates.”